How to retire without debt: Here’s how one couple did it

Updated Sept. 10, 2025, at 2:11 p.m. CT

Imagine entering retirement without the stress of monthly debt payments. That’s exactly what one longtime Dupaco Credit Union member set out to do—and his story shows it’s possible.

Since retiring, Chuck Andracchio has stayed active, enjoyed volunteering and spent more time outdoors with friends. He believes retirement is meant to be enjoyed. And being debt-free has helped make that possible.

“If I had debt in the back of my mind, it would be a burden,” he said.

Here’s how he and his wife prepared—and steps you could take if you want to retire debt-free too.

Why retiring with debt makes things harder

Carrying debt into retirement can be stressful.

Monthly payments for mortgages, credit cards or loans eat into your fixed income. That leaves less room for things like travel, hobbies, healthcare or even everyday living expenses.

“When people retire who aren’t financially prepared and don’t change their lifestyle, they tend to lean on credit cards to compensate for having a lower fixed income,” said Dupaco’s Jill Schweikert. “This leads to an increase in debt and tighter budgets.”

Going into retirement debt-free could mean:

- Lower monthly expenses

- More flexibility to handle rising costs (like healthcare or inflation)

- Greater peace of mind knowing you’re not locked into long-term payments

It doesn’t happen overnight. But with the right plan you could work toward it.

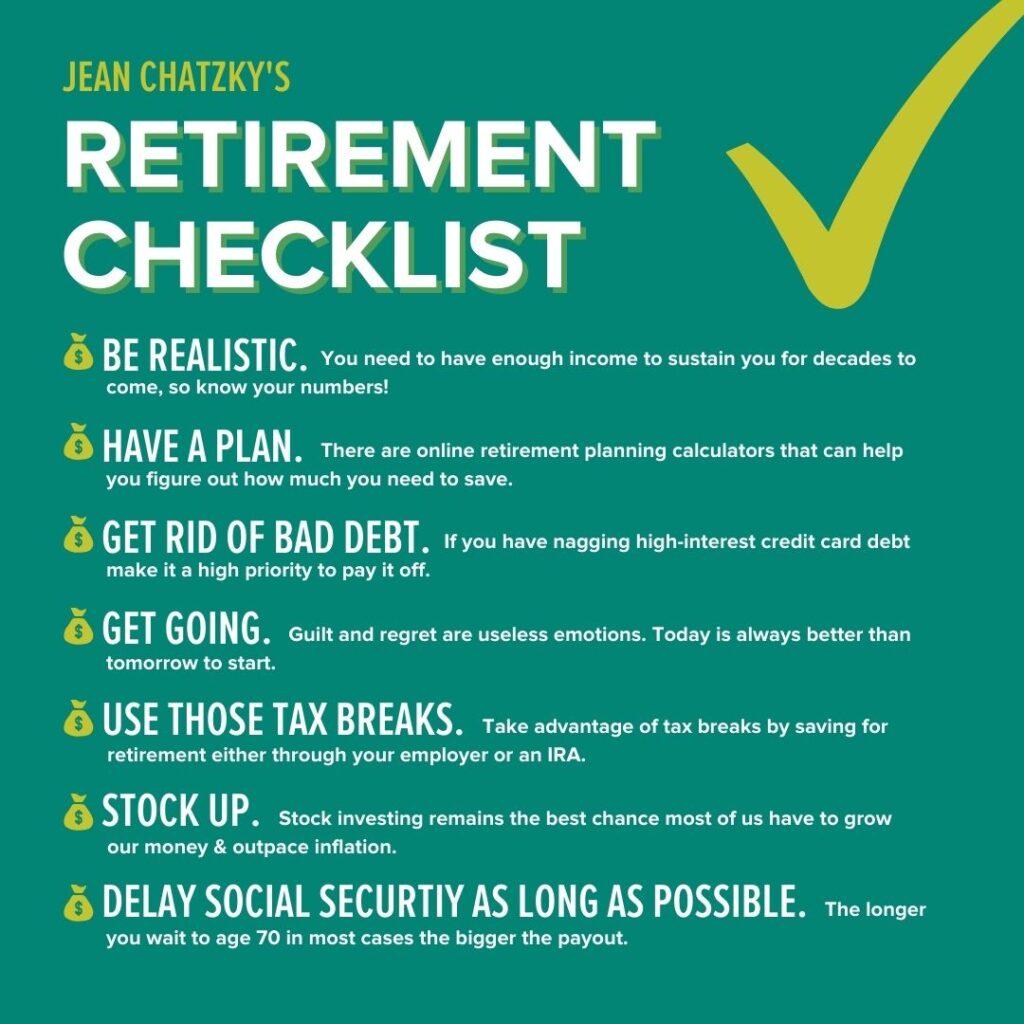

Start thinking about your ‘future self’

Enjoy the present—make memories and take some trips. But don’t forget about tomorrow (or a few tomorrows from now).

Chuck and his wife, Dawn, made a point to set aside money consistently.

Calculate how much you could save based on your income >

Here are a few practical ways to start:

- Build an emergency fund to avoid relying on credit cards for unexpected costs.

- Save in dedicated accounts like a You-Name-It Savings account, money market account, term-share certificates or Individual Retirement Accounts.

- Increase contributions as your income grows—even small changes add up.

“Hindsight is always 20-20,” Chuck said. “So many young people don’t take the time to think about the future. You really need to remember that there will be a day you’re going to be retired.”

Take full advantage of employee benefits

At every job he worked, Chuck contributed to his companies’ 401(k) retirement plans. His wife did the same.

Even if a company doesn’t match your contributions, it’s an opportunity to save for your future—with a bonus of potential tax benefits.

“You have to take advantage of those company 401(k)s,” Chuck said. “And if there’s any kind of a company match, that’s icing on the cake.”

Don’t have access to a workplace plan? You can still look into saving through an IRA or other accounts.

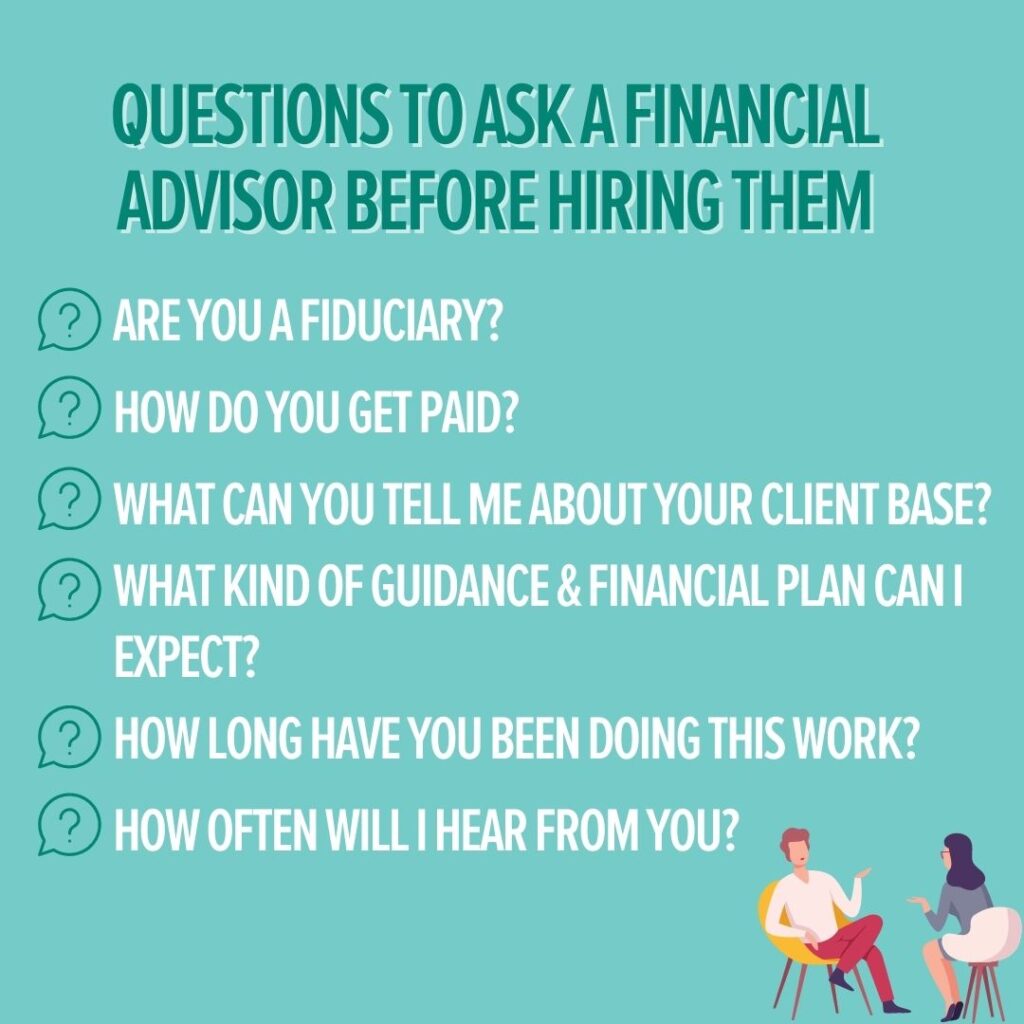

Work with a trusted financial advisor

Planning for retirement can feel overwhelming.

Chuck and his wife, Dawn, have worked with Suzan Martin-Hallahan, CFP®, a financial consultant at Dupaco Financial Services, for years. Together, they’ve created a plan tailored to their goals—and have stuck to it.

Every plan is different, which is why it’s important to be up front and honest with your financial planner about your goals and debts, Chuck said.

At first, their advisor encouraged them to slow down on extra debt payments so they could build an emergency fund for retirement.

Later, they were able to use that fund for unexpected expenses, vacations and even home updates.

“Having that fund available is a very comforting feeling,” Chuck said. “Retirement is really nice, especially when you have everything lined up personally as well as financially.”

Pay off your mortgage faster

One of the couple’s biggest priorities was paying off their mortgage before retirement. They did this by making biweekly payments instead of monthly ones.

Here’s why it works:

- With biweekly payments, you make 26 half-payments a year (the equivalent of 13 full payments instead of 12).

- That extra payment each year chips away at your principal faster.

- Over time, this can save you thousands in interest and cut years off your loan.

They also added extra principal payments whenever their budget allowed. Over time, those efforts added up to a debt-free home before retirement.

Plan for your health and happiness too

Planning for retirement isn’t only about money. It’s also about having purpose and staying healthy.

For Chuck, that meant joining a health club, volunteering and keeping active with hobbies.

“If you plan to retire, you better have something to do to occupy your time,” he said. “I see so many people … in great shape because they go and do something.”

Finding balance in retirement—between financial security and personal fulfillment—was key for him.

Final thoughts on retiring debt-free

Retiring without debt doesn’t happen by accident.

It takes planning, consistent saving and a willingness to stay disciplined. But as Chuck’s story shows, the payoff is worth it.

Start small: Build an emergency fund, take advantage of benefits, work with a trusted advisor and chip away at your mortgage.

Every step moves you closer to enjoying retirement on your terms—without debt weighing you down.

Your Dupaco Credit Union provides referrals to financial professionals of LPL Financial LLC (“LPL”) pursuant to an agreement that allows LPL to pay Dupaco Credit Union for these referrals. This creates an incentive for Dupaco Credit Union to make these referrals, resulting in a conflict of interest. Dupaco Credit Union is not a current client of LPL for brokerage or advisory services. Please read the LPL Financial Relationship Disclosure for more detailed information.

Dupaco Financial Services is a division of Dupaco Community Credit Union — the financial home you own — so you can rest assured that you're working with an organization that will act with your personal interest in mind. Dupaco Financial Services works with a national, full-service securities brokerage firm, LPL Financial, to make available top-of-the-line investment and insurance information and opportunities.

Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL Financial or its licensed affiliates. Dupaco Community Credit Union and Dupaco Financial Services are not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Dupaco Financial Services, and may also be employees of Dupaco Community Credit Union. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of, Dupaco Community Credit Union or Dupaco Financial Services. Securities and insurance offered through LPL or its affiliates are:

![]()

The LPL Financial Registered Representatives associated with this site may only discuss and/or transact securities business with residents of the following states: Iowa, Wisconsin and Illinois.