Zero-sum budgeting: How to give every dollar a purpose

Updated Sept. 5, 2025, at 12:07 p.m. CT

What if you could have a brighter financial future by spending every dollar you earned? Sounds counter-intuitive, right?

That’s the idea behind zero-sum budgeting—a method that makes you the boss of your money instead of wondering where it all went. With this approach, every dollar you earn has a specific job, whether that’s paying bills, building savings or enjoying life guilt-free.

In this guide, we’ll break down how zero-sum budgeting works, what makes it different from other budgeting methods and how to set one up for yourself.

What is zero-sum budgeting?

Zero-sum budgeting means you assign a purpose to every single dollar of your income until your monthly budget “totals zero.” That doesn’t mean you spend everything—it means your money is fully planned.

Here’s how it works:

- You use last month’s income to cover this month’s expenses.

- You give every dollar a “home” in your budget categories (rent, utilities, savings, debt repayment, fun, etc.).

- At the end of the month, nothing is left unassigned—your budget balances out to zero.

Think of it like telling your money where to go before it has a chance to wander off.

“If you don’t use every single dollar, you end up being tempted to spend that money on things you don’t really need,” said Dupaco Credit Union’s Erin Engler.

Engler has practiced zero-sum budgeting for as long as she can remember.

“It helps me save money and not be wasteful,” she said. “It also really helps me focus on getting my debts paid off quicker, and that saves me money in the long run too.”

Is zero-sum budgeting right for me?

Curious whether this budgeting approach would work for you? This method works best if you:

- Want more control over your spending

- Are focused on paying off debt

- Like a clear, structured system

- Have a fairly steady income (though gig workers can make it work too—see below!)

It might feel restrictive at first. But really, it’s about being intentional with your money so you can save more and stress less.

Step #1: Review your current budget

Before you dive in, you need to know where your money is going today. Write down:

- Monthly bills (rent, utilities, groceries)

- Semi-annual or annual expenses (insurance, memberships)

- Fun spending (subscriptions, hobbies, dining out)

“This is where people miss out. Make sure you know where your money is going and how much you’re paying in bills every month,” Engler said.

A free Dupaco Money Makeover could help you review where your money’s going, look for leaks in your budget and help you create a spending plan that’s right for you.

Step #2: Work with the bare minimum

If your paycheck varies (overtime, bonuses, commissions), create your zero-sum budget using your minimum guaranteed income. That way, you won’t overspend.

When extra income comes in, you can choose to:

- Pay down debt faster

- Add to savings goals (like vacation or home repairs)

- Build a financial cushion

Step #3: Use multiple accounts to stay organized

Zero-sum budgeting is easier when your money is organized. Instead of one big pot, try dividing funds across separate accounts:

- A checking account for everyday expenses

- Dedicated You-Name-It Savings accounts for goals like vacations, car insurance or home improvements

Dupaco lets you open multiple savings and checking accounts, so you can automatically set aside money for each budget category using either direct deposit or automatic transfers.

For example: Even if your car insurance is due every six months, you can transfer a little each paycheck into your “Car Insurance” savings account. When the bill arrives, you’re already prepared.

“Every single dollar of my paycheck has a home, whether it goes into a vacation savings account, car insurance account or something else,” Engler said.

Step #4: Account for variable expenses

Not every bill’s the same month to month. Your utility bill or grocery costs may fluctuate.

You have a couple options to help with these changes:

- Budget billing: Some utility companies average your usage so you can pay the same amount every month.

- Overestimate: Budget for the highest likely cost. If you come in under, roll the extra into savings or pay down debt.

Step #5: Monitor your budget and adjust regularly

Even with automation, check in on your budget.

Tools like Dupaco’s free eNotifier Alerts can help you track balances and spot unusual spending (plus protect you from fraud).

If you notice you’re always under in one category and over in another, simply reassign dollars so your budget balances back to zero.

Step #6: Pick the right time to start

Because you need one month’s income in advance, getting started can feel tricky.

You have some options to help you launch:

- Use a tax refund to get a month ahead.

- Start during a three-paycheck month if you’re paid biweekly.

- Save gradually until you can cover a month of expenses in full.

Step #7: Get on the same page

If you share finances with a partner, communication is key. Zero-sum budgeting works best when everyone knows the plan and agrees on where the money should go.

“If one person is really on top of your expenses and knows where your money is going and the other person doesn’t care, your budget isn’t going to be successful,” she said. “Everybody has to be on the same page.”

Pros and cons of zero-sum budgeting

Like any budgeting method, zero-sum budgeting has its strengths and challenges. Understanding both sides can help you decide whether it’s the right fit for your lifestyle.

Pros

- Every dollar has a purpose: You’ll know where your money’s going, which helps reduce wasteful or impulsive spending.

- Accelerates savings and debt payoff: By planning for both, you can make progress faster instead of hoping you’ll “have some left over.”

- Brings peace of mind: Having a plan in place reduces stress and makes unexpected bills less overwhelming.

- Works with digital tools: Using features in Shine Online and Mobile Banking makes it easier than ever to track spending, transfer money automatically and keep your budget balanced.

Cons

- Takes effort to set up: You’ll need to build a full month’s buffer of income before you can truly operate on last month’s dollars.

- Can feel restrictive: If you prefer flexibility or like spontaneous spending, zero-sum budgeting may feel too structured at first.

- Requires regular check-ins: While automation helps, you’ll still need to review and adjust as bills, income or goals change.

- Best with steady income: If your income is highly irregular, it takes more planning and discipline to make this method work smoothly.

The key takeaway? If you like structure, want to eliminate financial guesswork and are motivated to save or pay down debt, zero-sum budgeting can be a powerful tool. But if your income is unpredictable or you prefer looser guidelines, you may want to try a hybrid approach—using zero-sum for core expenses and a more flexible budget for the rest.

Zero-sum budgeting vs. other methods

Zero-sum budgeting isn’t the only way to manage your money.

If you’re not sure whether it’s the right fit, it helps to compare it with other popular approaches:

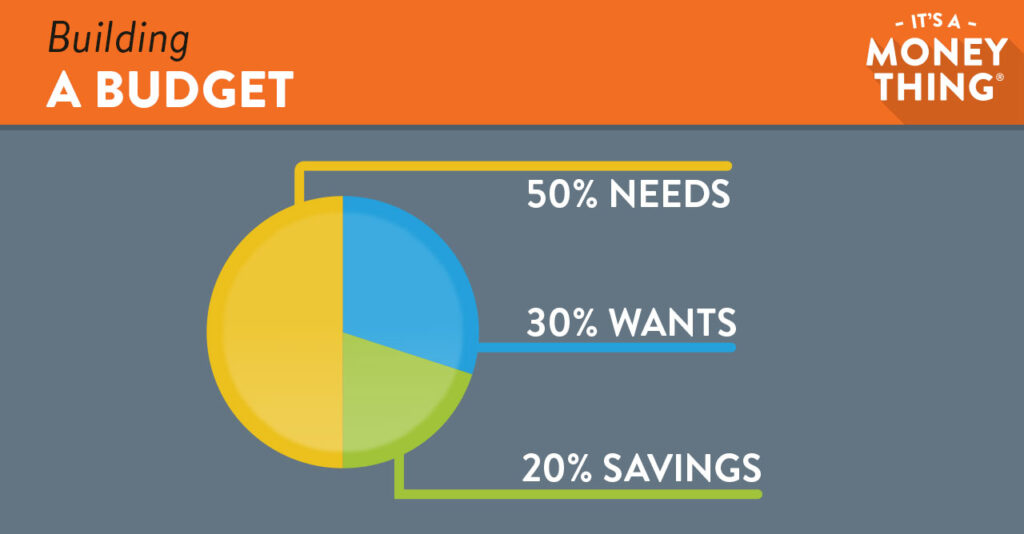

- 50/30/20 budget: A simpler method where 50% of income goes to needs, 30% to wants and 20% to savings or debt. It could be easier to maintain but doesn’t give the same level of detail and control as zero-sum budgeting.

- Envelope system: The old-school, cash-in-envelopes method. It forces discipline but can be inconvenient in today’s mostly digital world. Zero-sum budgeting is essentially a modern, digital version using accounts and transfers instead of paper envelopes.

- Pay-yourself-first method: This approach prioritizes savings before spending on anything else. It works well if saving is your main goal, but you might lose track of where the rest of your money is going without a fuller system.

Zero-sum budgeting combines the control of the envelope system with the flexibility of digital tools, while still keeping savings front and center.

The bottom line

Zero-sum budgeting isn’t about spending all your money. It’s about assigning it wisely, so your priorities get funded first. Whether you’re focused on debt payoff, saving for your first home or planning for retirement, this method can give you peace of mind.