Home equity loan or line of credit: Which is right for you?

Updated Dec. 13, 2025, at 2:11 p.m. CT

Your home can be a powerful asset long before you sell it. By borrowing against the equity you’ve built in your house—through either a home equity loan or home equity line of credit (HELOC)—you could consolidate debt, fund home improvement projects or cover other big expenses.

But many homeowners wonder: “Which one is right for me?”

The answer really depends on your situation.

Let’s walk through what these loans are, how they’re alike, where they differ and when one might work better than the other.

What is home equity, and how do you build it?

Home equity is the difference between your home’s current fair market value and what you still owe on it. In other words: It’s the part of the house that belongs to you—not your lender.

Your equity should grow over time as you pay down your mortgage balance. You can speed this up by making biweekly payments. When you pay down your balance every other week, you end up making one extra monthly payment each year—ultimately owning even more of your home.

Your equity may also increase if property values in your neighborhood rise.

How are home equity loans and HELOCs similar?

A home equity loan and a home equity line of credit let you tap into the equity in your home while you still live there.

Both types of loans are considered a second mortgage on your house. With both, you’re borrowing against your equity. You’re using your home as collateral, which helps protect your lender. That means if you default on your loan, your lender can seize your home and sell it to attempt to recoup its losses.

Because you’re using your home as collateral, these loans typically come with much lower interest rates than personal loans or credit cards.

Once you have a home equity loan or home equity line of credit, you can use the funds for whatever purpose you choose. Here are a few ways homeowners use them:

- Debt consolidation: Transfer and combine your loan and credit card balances into one loan, potentially lowering your interest and monthly payment.

- Home improvements: Some projects, like a kitchen or bathroom remodel, can add comfort and increase the value of your home—in turn boosting your equity.

- Covering another big expense: Use the funds for an emergency, medical bills or even as a safety net for the unexpected.

Either loan will show up on your credit report as another open trade line. If you maintain a positive payment history on your loan, it could help strengthen your credit score.

You’ll need to consult your tax advisor to determine whether you’ll qualify for a tax deduction with a home equity loan or home equity line of credit.

Estimate the impact of consolidating debt >

How are home equity loans and HELOCs different?

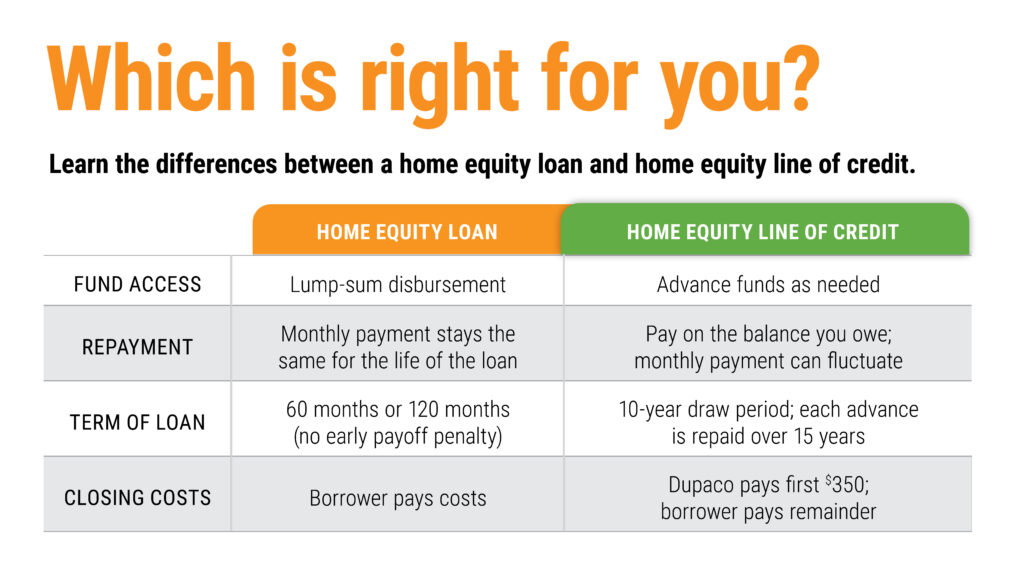

While a home equity loan and home equity line of credit share similarities, their terms work quite differently. Here’s a breakdown of the main differences between Dupaco’s two home equity options.

How you access the funds

- Home equity loan: You get the funds in one lump-sum—regardless of whether you need all of it at that time.

- HELOC: You withdraw funds as needed. You can access the money through Shine Online or Mobile Banking, by calling Dupaco at 800-373-7600, visiting a Dupaco branch or writing a check from your HELOC account.

Repaying the funds

- Home equity loan: Your monthly payment remains the same throughout the life of the loan, which is a 120-month (10 years) or 60-month (five years) term. At Dupaco, you have the option to make weekly or biweekly payments to pay off the loan faster.

- HELOC: Repayment works kind of like a credit card. You borrow what you need up to your limit, repay it and borrow again. You have 10 years to withdraw money from your line of credit. Each advance has its own 15-year repayment schedule. In theory, you could leave the line of credit untouched for nine years, take a full advance at that time and then have 15 more years to repay those funds. Unlike a home equity loan, your monthly payment can change, triggered each time you make an advance.

Interest rates

- Home equity loan: It’s a fixed interest rate, which means your payment never changes.

- HELOC: You’ll pay a variable interest rate, which is based on the Prime Lending Rate. Your payment only changes when you take a new advance.

Closing costs

- Home equity loan: You pay the closing costs.

- HELOC: Dupaco pays up to $350 of your closing costs. You’re responsible for any remaining balance.

Calculate what a HELOC payoff might look like >

When does a home equity loan make the most sense?

Depending on your needs, one loan will likely work better for you than the other. A home equity loan might be your best option if you:

- Know exactly what you want to use the funds for and know how much money you need (for example, a $30,000 kitchen remodel).

- Prefer the predictability of knowing exactly how much the payment will be each month.

- Want a shorter repayment schedule to get debt off your plate sooner (some homeowners appreciate this).

Because the payment is the same every month, home equity loans can make it easier to budget without surprises.

When is a HELOC a better option?

A HELOC might be right for you if you:

- Want flexibility to borrow only what you need, when you need it.

- Like the idea of a safety net. Maybe you don’t have a specific expense in mind—or are unsure if you might have other needs down the road.

- Appreciate a long draw period (10 years), especially for ongoing costs like phased home improvements.

What should you watch out for with either option?

Remember, you’re taking out a second mortgage on your property. That means your home is used as collateral. Anytime you consider doing this, think carefully about why you’re doing so. Here are a few tips to keep in mind:

- It’s even more important to make your payments on time, every time—missing them could put your home at risk.

- If you plan to sell your home, you’ll need to pay off your home equity loan or line of credit paid in full first.

- Variable interest rates on HELOCs mean your payments could rise when you take an advance if market rates go up.

Final thoughts: Which is right for you?

Ultimately, choosing between a home equity loan and a HELOC comes down to personal preference, needs and comfort level.

- Want certainty and a fixed repayment schedule? A home equity loan might be the best fit.

- Prefer flexibility and ongoing access to funds? A HELOC could be the smarter choice for you.

Through careful planning, a home equity loan or line of credit can be a powerful way to tap into the equity you’ve built.