How to lower the cost of college tuition: Smart ways to save

Updated on Sept. 8, 2025, at 3:30 p.m. CT

College tuition keeps climbing. But that doesn’t mean you have to be stuck with overwhelming debt. The truth is, with a little planning and creativity, there are ways to bring down the cost of a degree.

Whether you’re a student figuring out how to pay for school or a parent trying to support your child’s education, the right mix of strategies can add up to thousands in savings.

For many young adults, student loans serve as the first real experience with borrowing a large amount of money.

Here are some practical ways to lower your total tuition bill—and reduce how much you’ll need to borrow later.

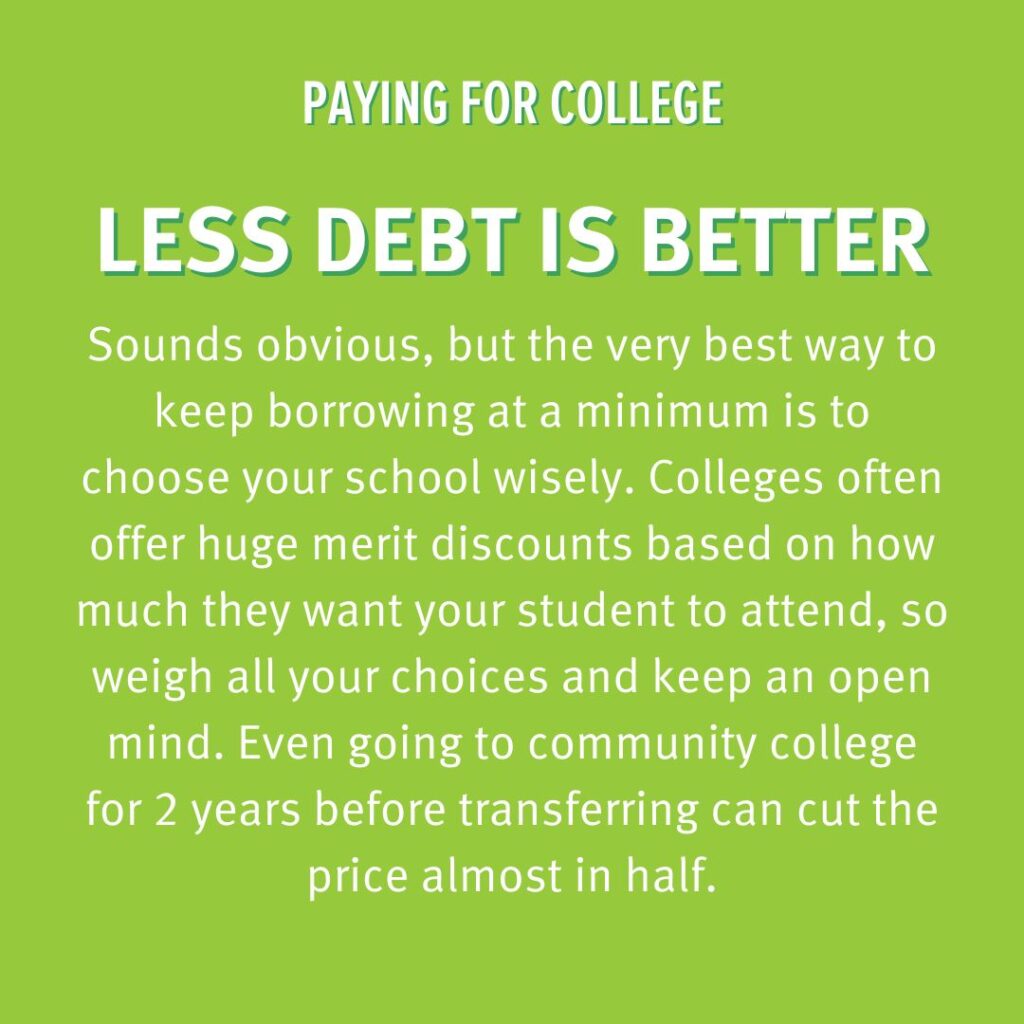

|1| Start at a community college

Taking general education courses at a local community college can save thousands compared to starting at a four-year university.

Many students complete an associate’s degree first, then transfer to their school of choice to finish their bachelor’s. This way, you save some money on introductory-level courses and reserve the big bucks for the specialized instruction.

|2| Earn college credits in high school

Find out if there are any opportunities to earn college credits while still in high school.

Beyond reducing college tuition costs, advanced college credit programs are an excellent way to explore your interests more seriously and get a sneak preview of what your college workload will look like.

If you’re already out of high school, find out if any colleges or universities in your area offer summer courses at reduced tuition. That could be an alternative way to score some credits before September.

|3| Compare financial aid packages carefully

Not all aid offers are created equal.

One school might look more expensive on paper but provide a stronger mix of grants and scholarships. Another might lean more heavily on loans.

Look beyond the “sticker price” and calculate your net cost.

|4| Search wide and often for scholarships and grants

Free money is out there—you just need to dig for it. Here are a few places to start:

- Your high school guidance counselor

- Financial aid office at colleges you’d like to attend

- Reputable scholarship search engines

- Ask employers, community organizations or alumni networks

Be exhaustive in your search and approach. Even small awards add up, especially when you stack them.

Treat scholarships like a part-time job: Apply to as many as possible, and keep at it year after year.

Check out the Dupaco Foundation’s need-based college scholarships >

|5| Consider in-state schools or ones that waive out-of-state fees

Where you go to school matters as much as what you study.

In-state tuition is often far more affordable than out-of-state or international options. Some universities also have special agreements that reduce or waive out-of-state costs.

Choosing location strategically can save you not only on tuition but other costs like:

- Travel

- Housing

- Meal plans

Of course, there are plenty of non-financial incentives for studying abroad. But it’s important to understand just how much the location of your school will affect your bottom line.

|6| Accelerate your degree

Some schools offer accelerated programs that let you complete a four-year degree in just three years.

This can be a great option to consider. That’s one less year of tuition to pay! But keep in mind that you’ll be squeezing more classes into a shorter period of time. The intensive schedule might make it difficult to accommodate a job while you’re in school, so weigh whether it’s realistic to balance classes, work and personal life.

|7| Make the most of work-study and part-time jobs

Working during school doesn’t just provide income—it can also lower how much you need to borrow.

Federal work-study programs often connect students with campus jobs, while part-time positions in your field of study give you both a paycheck and career experience. Even 10 hours per week can make a difference.

|8| Use 529 savings plans and family contributions wisely

Parents: If you’ve set aside funds in a 529 plan or similar savings account, this is the time to put them to use.

These accounts offer tax advantages and can be a smart way to reduce reliance on loans.

If you’re still in the saving stage, it’s not too late to start—even a year or two of contributions can offset some costs.

|9| Consider appealing your financial aid offer

Financial aid decisions aren’t always final. If your family’s income has changed, medical bills have piled up or another school has offered a better package, you can write a formal appeal.

Colleges sometimes reconsider and provide additional aid when asked.

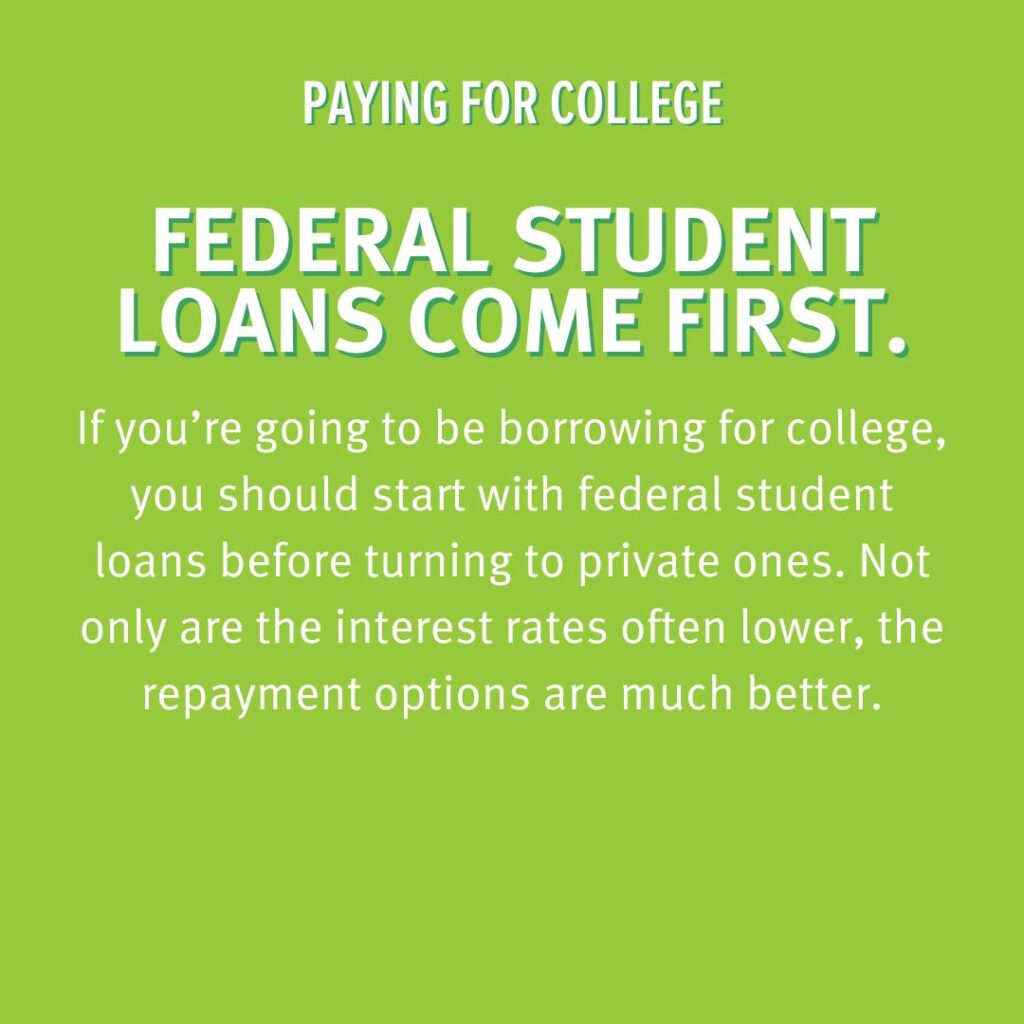

|10| Borrow only what you truly need

Even with scholarships, savings and financial aid, you may still need to borrow to cover the remaining cost of tuition. If that’s the case, start with federal student loans, since they usually come with lower interest rates and flexible repayment options.

But what if federal aid and scholarships still aren’t enough? That’s where private student loans can help fill the gap. The key is to borrow responsibly:

- Only take what you need to cover tuition and essential expenses.

- Understand the interest rate, repayment terms and how much your future monthly payment will be.

- Compare lenders and choose a trusted financial institution that prioritizes your long-term financial health.

Explore Dupaco’s student loan program >

A note for parents

Balancing college costs with your own financial goals can be tough.

You want to support your student without sacrificing retirement savings or other priorities. If you’re unsure how to strike that balance, consider talking with a financial expert.