When does it make sense to refinance student loans?

If you’ve started to repay student loans, the cost of your education has probably become even clearer. And maybe even a little overwhelming. You...

4 min read

Not sure if refinancing is the right move? In this guide, we’ll cover:

Here’s how to know if refinancing might make sense for you.

When you refinance your auto loan, you replace your current loan with a new one. The new loan pays off the remaining balance of your old loan, and you start fresh with new terms. This could mean a lower interest rate, a different loan length or a lower monthly payment.

The process is often simple and fast, and you don’t change vehicles to refinance.

People refinance their car loans for different reasons. Here are some of the most common:

Depending on your situation, one or more of these reasons might apply. Here are some scenarios where refinancing could be a smart move:

If market rates have gone down since you originally financed your vehicle, refinancing could help you secure a better rate and offer significant savings over the life of the loan.

Stronger credit could potentially open the door to better rates and loan terms.

Many people feel rushed during the car-buying process and end up with financing that wasn’t the best deal.

Life changes. Whether your budget has tightened or improved, refinancing allows you to adjust your payment to better fit your current needs.

If you’ve built up some equity in your vehicle, refinancing could give you an opportunity to combine higher interest debts—like credit cards or personal loans—into one lower-rate payment.

It’s a way to simplify what you owe and potentially save on interest, especially if your auto loan rate is much lower than your other balances.

Just keep in mind that spreading out your debt over a longer loan term could impact the total interest you pay, so it’s worth doing the math to see if it fits your financial goals.

See other debt consolidation options >

Life doesn’t always go according to plan—and that can be stressful when you have a loan to think about.

If you’re thinking about refinancing, it can also be a good time to consider how you’d handle unexpected bumps in the road—like a job loss, illness or damage to your vehicle.

Loan protection isn’t for everyone, but some people find peace of mind in having a backup plan. Depending on what you choose, protection could help cover your loan payments during tough times or help pay off your loan if your car is totaled or stolen.

It’s worth exploring the options and weighing the cost against the potential benefit.

Explore loan protection options >

Refinancing isn’t always the right move. Here are some reasons you might want to hold off:

Everyone’s situation is different, but a State of Auto Refinance: 2022 report show that:

Try our auto loan refinance calculator >

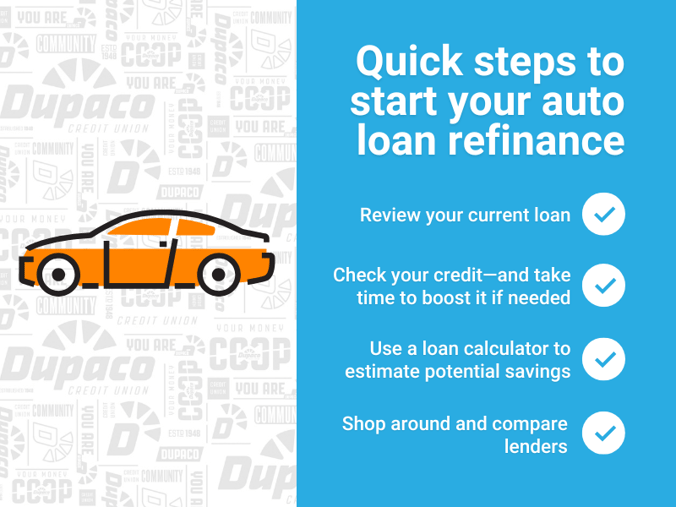

Ready to see if refinancing makes sense for you? Here’s how to get started:

If your score has improved since you took out your original loan, you may qualify for better rates. If you’re a Dupaco member, you can view your score anytime with our Bright Track Credit Monitoring—a free tool in Shine Online and Mobile Banking.

Not sure where to start? A free Credit History Lesson could help you learn how to build your credit!

See how refinancing could change your payment—and how much you might save—with a tool like Dupaco’s free auto loan refinance calculator.

Hint: You’ll want to know some details about your existing loan before you get started:

Even a small difference in rates can add up.

If your financial situation has changed since you bought your car, refinancing your auto loan could benefit you. Take a few minutes to review your current loan—and see if a better deal is out there.

Why it’s worth a look:

If you’re unsure, a Dupaco financial expert can help you explore your options and build a plan that fits your budget, goals and timeline.

If you’ve started to repay student loans, the cost of your education has probably become even clearer. And maybe even a little overwhelming. You...

Your mortgage payment is likely one of your biggest monthly expenses. But what if you could get a do-over on your loan to lower your payment, pay off...

Refinancing your mortgage before retirement is a big decision. The right move depends on your goals, finances and how long you plan to stay in your...